The 30-Year Mortgage at 6%? It's a Launchpad, Not a Ceiling

Okay, folks, let's talk numbers. I know, I know, finance can feel like staring into a spreadsheet abyss, but trust me, there's a shimmering oasis of opportunity hidden in today's mortgage rates. The headlines are all "Mortgage rates dip slightly!" or "Mortgage and refinance interest rates today, November 25, 2025: Lowest 30-year rate this year!" and while that's factually correct, it's missing the forest for the trees. It’s like saying the Wright brothers achieved a “brief, controlled glide” while completely ignoring the fact that they invented flight!

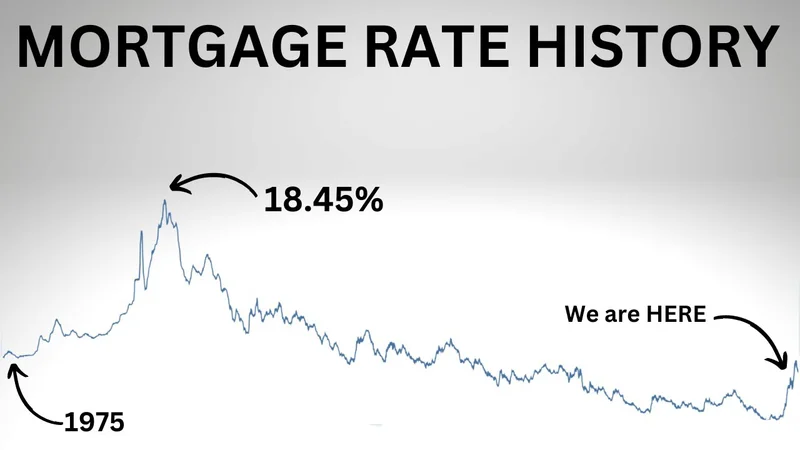

Yes, the average 30-year fixed-rate mortgage is hovering around 6.06%, give or take a few basis points. And yes, that's the lowest we've seen in a while. But what does that really mean? It means the engines are primed. The launch sequence has begun. We're not just talking about buying a house; we're talking about building a future.

Why This Isn't Just About Homeownership

See, the key here is to understand that these rates aren't just numbers on a loan application. They're signals. They're indicators of a market that's stabilizing, a Federal Reserve that's (finally!) starting to ease up, and an economy that's slowly, painstakingly, recalibrating. The Fed decreased its rate in late 2024 and has cut it twice in 2025, including at its latest meeting on October 29. They are even considering another cut before year's end.

Think of it like this: the housing market is a giant flywheel. For the past few years, it's been stuck, grinding against the friction of high rates and economic uncertainty. Now, that flywheel is starting to turn. And once it gets going, it generates momentum. It creates opportunities for builders, for renovators, for entrepreneurs, for all of us.

And that’s before we even talk about the impact on individual families. Imagine a young couple, finally able to afford their first home. Suddenly, they have a stable foundation, a place to build memories, to raise a family, to invest in their community. It's not just about four walls and a roof; it's about security, stability, and the chance to pursue their dreams.

But it's not just about first-time homebuyers. Lower rates also mean opportunities for existing homeowners to refinance, to free up cash flow, to invest in their businesses, their education, their future. It's a chance to breathe, to innovate, to create.

And let's be honest, it's been a tough few years. We've all felt the pinch of inflation, the uncertainty of the market, the weight of the world on our shoulders. This slight dip in mortgage rates? It's not a solution to all our problems, but it's a glimmer of hope. A sign that things are starting to move in the right direction.

Here's my first-person moment of pure excitement: When I see these little shifts in the market, I don't just see numbers. I see families realizing their dreams. I see entrepreneurs launching new businesses. I see communities thriving. It reminds me why I got into this field in the first place. To help people build a better future.

Of course, there's a responsibility that comes with all this. We need to be smart about how we use this opportunity. We need to be mindful of our debt, to invest wisely, and to support policies that promote sustainable growth. But let's not let caution paralyze us. Let's embrace this moment with optimism, with creativity, and with a shared commitment to building a brighter tomorrow.

The question I keep asking myself is, how can we leverage this moment to create even more opportunities? How can we ensure that everyone has access to affordable housing, to capital, to the resources they need to thrive? These are the questions we need to be asking, the challenges we need to be tackling.

And what about the future? Well, economists are cautiously optimistic. They don't expect drastic rate drops before the end of the year, but they do anticipate a gradual easing in 2026. But even if rates stay relatively stable, the fact that they're not skyrocketing is a win. It's a sign that the market is finding its footing, that the worst may be behind us.

We also need to remember the human element. As one article rightly points out, real estate agents are more capable advisors for clients when they look into readily available market data. The current uncertainty about all factors affecting property value is best resolved by considering information about the behavior of real estate consumers.

This is Our Moment to Build

This isn't just about buying a house. It's about investing in ourselves, our communities, and our future. It's about turning a small dip in mortgage rates into a giant leap for mankind. So, let's get to work!